The stablecoin-plus-4626-vault protocol has become a template: ABC for the peg, sABC for the yield, points that convert into a governance token nobody really governs with. I argue that token is mispriced by design — and sketch two ways to fix it.

By the middle of 2026, most DeFi protocols fall into one of two families. The first builds infrastructure or runs a real business — Pump.fun, the spot DEXs, the perp DEXs. These throw off genuine cash flow that rises and falls with market heat and their own growth. The second family is what I'll call the yield-dividend protocol: a stablecoin wrapped around an ERC-4626 vault, where the returns come from basis trades (Ethena's USDe, Falcon's USDf) or from real-world assets (USDai, reUSD, tokenized Treasuries). The playbook is identical — raise money from crypto, deploy it somewhere that earns, then repackage that yield into a product that pays a little more than a T-bill and sell it back to the market.

This article is about that second family, and one uncomfortable question: do these protocols even need a token?

The Yield-Dividend Template

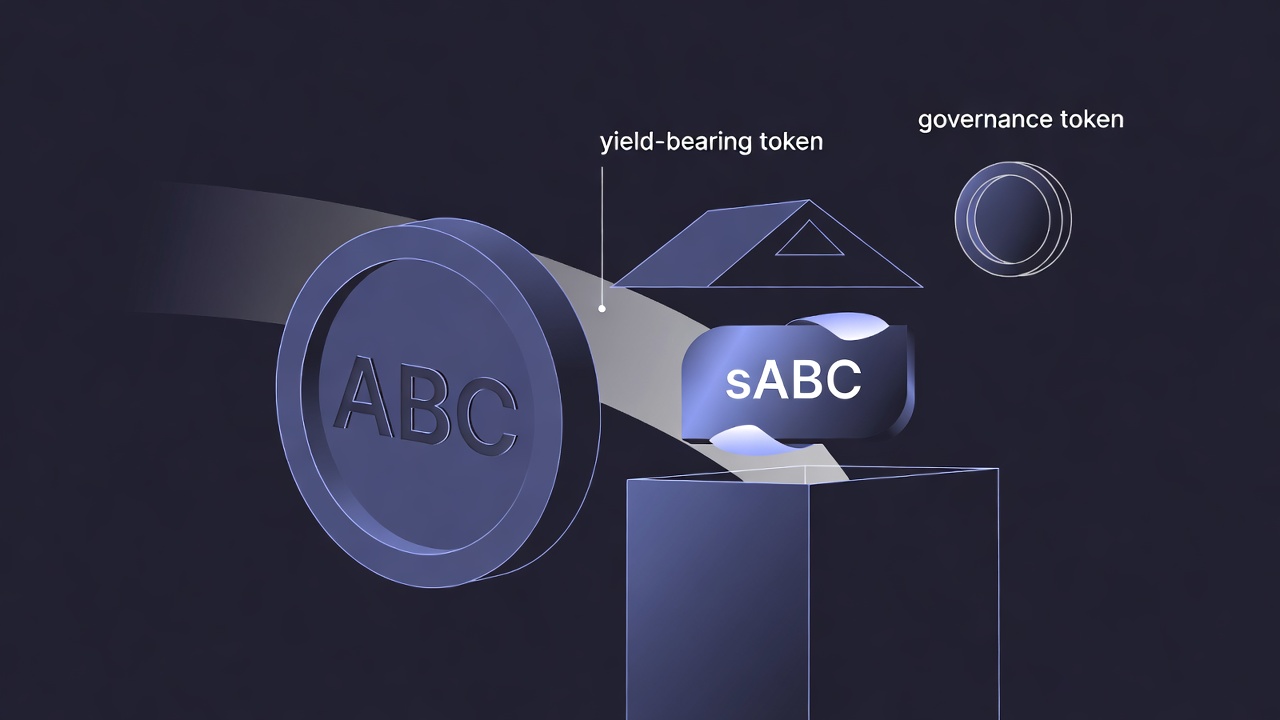

These protocols look like they were stamped out of the same mold. There's a stablecoin — call it ABC — and a yield-bearing wrapper, sABC. Hold ABC and you earn nothing (maybe some points). Stake into sABC and you collect a steady 5–20%, depending on what the underlying assets are — and, correspondingly, you eat the blow-up risk of those assets if they fail.

To pull in deposits, the team runs a points program. Early contributors — people who provide DEX liquidity, build Pendle LP positions, buy YT to farm points — accrue points that convert, a few seasons later, into the protocol's token. Ecosystem incentives usually hand out 10–30% of total supply this way. The rest is split among investors, the team, listing fees, and marketing. That's the whole machine.

| Infrastructure / business protocol | Yield-dividend protocol | |

|---|---|---|

| Examples | Hyperliquid, Pump.fun, spot & perp DEXs | Ethena (USDe), Falcon (USDf), USDai, reUSD |

| Revenue source | Trading fees, launch fees — scales with usage | Basis trades / RWA yield — scales with TVL |

| What the user holds | The token, or nothing | sABC (the yield wrapper) |

| Where yield goes | Often buybacks (see below) | The 4626 vault, by construction |

| Why the token exists | Captures business growth | ...that's the question |

The template: ABC holds the peg, sABC carries the yield — and the governance token drifts off to the side, attached to neither the vault's cash flow nor much real control.

The template: ABC holds the peg, sABC carries the yield — and the governance token drifts off to the side, attached to neither the vault's cash flow nor much real control.

Do These Tokens Even Need to Exist?

Picture a listed company running a profitable business — selling a product, booking a little money every year. If the business is growing fast, that growth shows up in the share price. But take an old, boring business: a phone company like AT&T, a burger chain like McDonald's. These have been around for a century. The stock barely moves; the company just pays a dividend, and 3–5% is a respectable one. So a shareholder cashes out their return two ways — price appreciation or dividends. Who decides what the company actually does — open a new line, kill an old one? A board and a shareholder meeting. But the ordinary investor has no operational say; they read the filings and that's it, unless they own enough stock to take a board seat.

Now map that onto a DeFi protocol. Governance runs through DAO voting, ostensibly one-token-one-vote — coin equals share, share equals vote. Except in practice, DeFi governance is often close to powerless. A proposal passes, a smart contract executes it — but the contract is code the team wrote, and what powers the DAO even has were decided by the team in the first place. The governance token votes inside a fence the team built.

Governance Tokens Barely Govern

If that sounds abstract, 2026 gave us two concrete illustrations.

The first is the fight between Aave Labs and the Aave DAO. Late in 2025, Aave Labs — Stani Kulechov's development company — swapped the swap provider on aave.com to CoW Swap and kept the fees, lifting interface swap revenue from roughly $1.1M to about $10M annualized, but routing it away from the DAO treasury. When delegates pushed back, Kulechov argued Labs had built and run the interface for eight-plus years and publicly called the claim that Labs owed the DAO a fiduciary duty "nonsense." A rushed December 22 Snapshot to move brand assets — the domain, socials, GitHub — into a DAO-controlled entity was voted down, and critics accused Kulechov of a "governance attack" after he bought roughly $10M of AAVE shortly before a vote (an allegation, not an established fact). It only resolved in April 2026, when the binding "Aave Will Win" vote passed with ~75% support: the DAO handed Labs $25M plus 75,000 AAVE to fund V4, in exchange for Labs routing branded-product revenue back to the treasury. Along the way two major contributor groups — the Aave Chan Initiative and BGD Labs — walked away, citing the team's growing grip on governance outcomes. The takeaway isn't that anyone was a villain; it's that even on the flagship DAO, the team held the real leverage and the token holders had to negotiate for scraps of the revenue their own protocol produced.

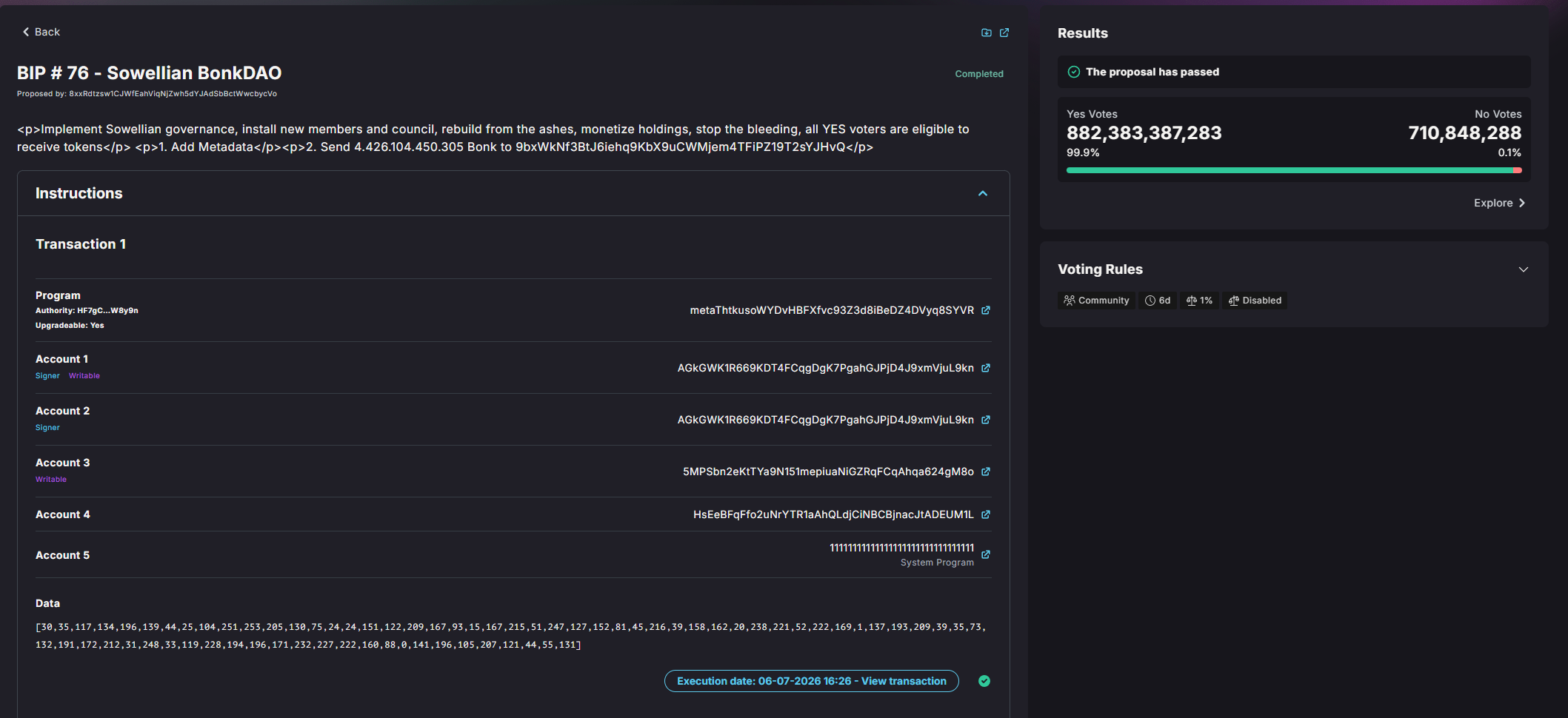

The second example is darker and more absurd. In July 2026, an attacker drained roughly $20M from BonkDAO's treasury — not by exploiting a bug, but by following the rules. They spent about $4.4M buying just over 1% of BONK's supply, enough to control ~99.9% of the votes actually cast, then submitted proposal "BIP #76" to move the treasury to their own wallet. It sat open for about six days. When it executed on July 6, only seven wallets had voted; more than 18,000 members — a ~2.9% turnout — simply didn't show up. It's the on-chain equivalent of a healthy democracy where nobody bothers to vote, so a single bad actor quietly registers, wins, and dissolves the parliament on day one. Twenty million dollars walked out in broad daylight. Notably the funds went mostly to a fresh multisig, with only a sliver cashed out to an exchange — no mixer, no tumbler. Observers debated whether this was even "theft" or just someone exploiting a mechanism everyone else ignored. That debate is the whole point: the decentralized governance people spent years lionizing turned out to be something almost nobody was watching.

BonkDAO's BIP #76 — "monetize holdings," then "Send 4.426.104.450.305 Bonk" to the proposer's own wallet. It passed with 99.9% of the vote after six days open, and executed on 06-07-2026. Every field is valid; that's what makes it unsettling.

BonkDAO's BIP #76 — "monetize holdings," then "Send 4.426.104.450.305 Bonk" to the proposer's own wallet. It passed with 99.9% of the vote after six days open, and executed on 06-07-2026. Every field is valid; that's what makes it unsettling.

So if the governance token barely governs, does it at least pay?

The Value-Capture Mismatch

Infrastructure protocols sometimes share revenue and sometimes don't. Hyperliquid funnels the vast majority of its fees — commonly reported around 97%, with 2026 figures cited near 99% — into an automated buyback-and-burn of HYPE through its Assistance Fund. Pendle directs up to 80% of protocol revenue into PENDLE buybacks that fund distributions to stakers. Pendle does one thing I genuinely admire: under its 2026 sPENDLE model, a staker who fails to vote during an active governance proposal window has their rewards paused for two weeks. No participation, no yield. That actually makes sense — it ties the reward to the behavior the token is supposed to buy.

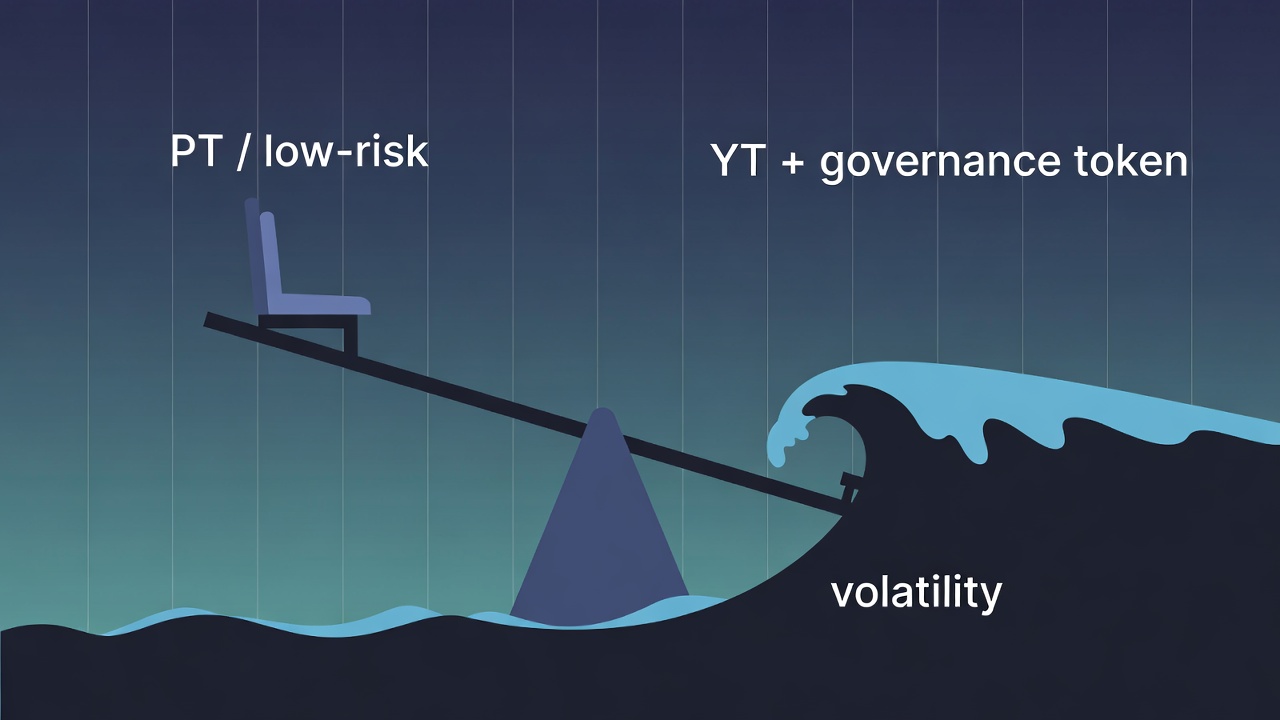

The yield-dividend protocol is where it gets awkward, because the yield is already spoken for — it all flows to the 4626 vault. Some teams skim a slice of that yield for operating costs, and maybe a further slice to the governance token. But the tension is structural, not incidental: governance and cash flow live on different channels. The token has little governance power and little revenue right, so it drifts into being a meme — a bet that someone later will pay more for it. Meanwhile the person who just wants steady income buys the PT on Pendle and locks a fixed rate at almost no risk. As it stands, buying the PT of a yield protocol is close to low-risk, high-return — and the risk that PT sheds has to land somewhere. It lands on the YT holders and the governance-token holders. That's the mismatch: the safest seat pays well, and the token that's supposed to represent the protocol absorbs the volatility with neither the control nor the dividend to justify it.

The safe seat sits high and dry; the YT and governance-token holders slide into the volatility. Risk shed by the fixed-rate PT has to land somewhere.

The safe seat sits high and dry; the YT and governance-token holders slide into the volatility. Risk shed by the fixed-rate PT has to land somewhere.

I want to sketch two ways out.

Structure One: Retire the Governance Token

The simplest fix is to not launch a token at all. Plenty of these protocols don't need one. Pay a clean, steady dividend; let the team take a fixed 10–20% of yield as the cost of running the shop. Governance is barely worth anything anyway — if you want a vote, vote with your 4626 stake token directly. The relationship becomes simple and honest: users are there for yield, the founders grow the pie, everyone splits a bigger pie. To bootstrap the early ecosystem the team can dial its cut down, then raise it slowly as TVL grows.

The catch is venture capital. If the project took VC money, this path is hard — most VCs want to realize returns through a token launch, not by waiting years for the business to mature and pay more. A no-token protocol is a great deal for users and a bad exit for the cap table.

Structure Two: Migrate Yield from Vault to Token, Season by Season

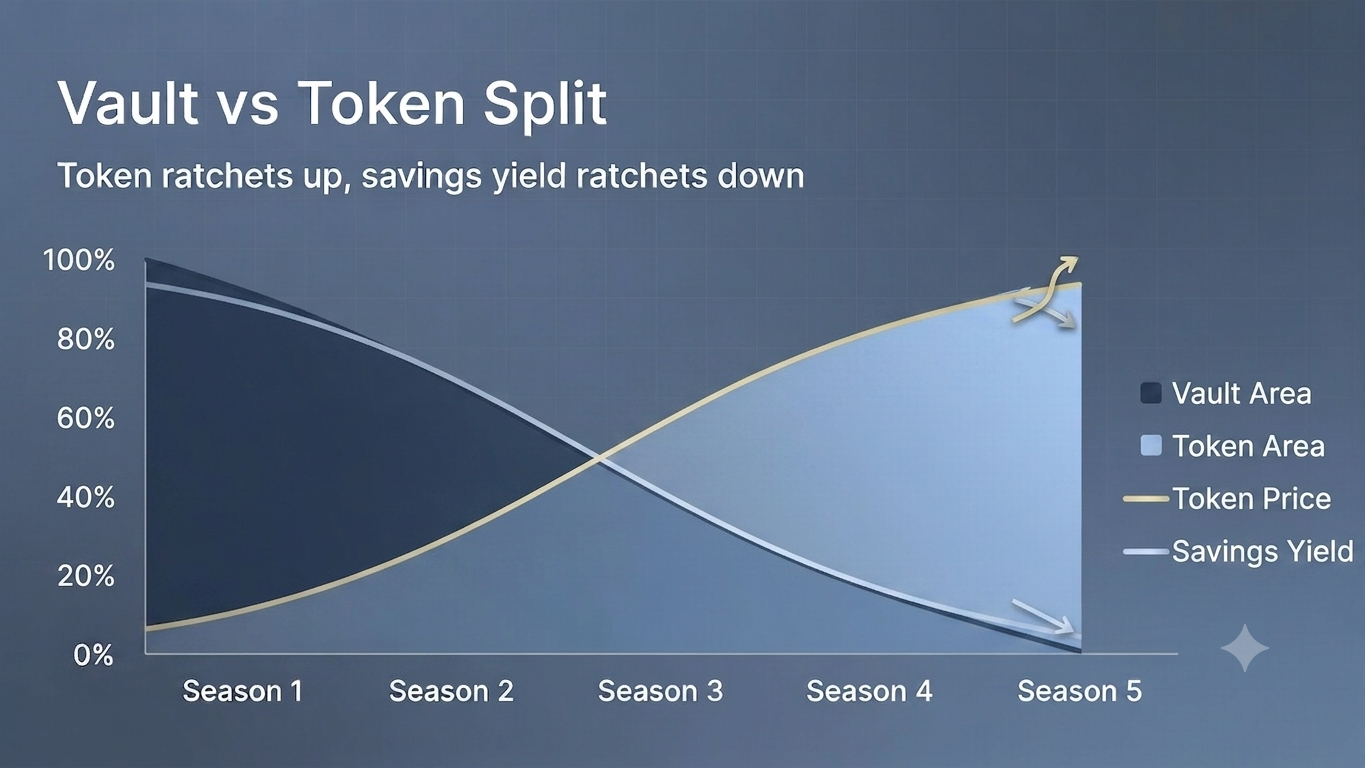

The second structure keeps a token but turns it into something closer to real equity. Early on you still need incentives, so you still run points to bootstrap TVL and hand a slice of tokens to early farmers — who are free to sell. But you also announce a five-season transition, and across those seasons the team steadily shifts the yield stream from the 4626 vault to the governance token.

Say the protocol earns $100. Today the vault takes $95 and the team takes $5. Under the transition, each season moves the split further toward the token:

| Season | Yield to 4626 vault | Yield to governance token |

|---|---|---|

| 1 | 100 | 0 |

| 2 | 80 | 20 |

| 3 | 60 | 40 |

| 4 | 40 | 60 |

| 5 | 0 | 100 |

The crossover: the vault's cut of the yield ratchets down while the token's ratchets up, season by season, until the token captures all of it.

The crossover: the vault's cut of the yield ratchets down while the token's ratchets up, season by season, until the token captures all of it.

By the end, all $100 accrues to the token. The team no longer skims the yield — it holds a designed allocation of the token instead, so its share of the profit comes from the same place everyone else's does. During the transition, the points the vault farmers earned convert into that token. The net effect: most people stop buying a plain, stable savings product and instead hold the token — a share-like instrument that carries both governance and a dividend right. The team buys back and burns with the revenue, or buys back and distributes to stakers. The exact tokenomics need careful tuning, but the direction is clear: turn the governance token into genuine equity — control and profit — instead of a claim on neither.

If TVL grows steadily and revenue with it, the token price should ratchet up while the stable-savings yield ratchets down, until the plain product is fully phased out.

The Trade-offs

Neither structure is free. Here's how the three models stack up:

| Today's yield-dividend token | Structure 1: no token | Structure 2: migrate to equity | |

|---|---|---|---|

| Governance power | Nominal — votes inside the team's fence | Vote with vault stake, or don't | Real, backed by cash flow |

| Revenue right | Little to none | Steady dividend via the vault | Full — all yield accrues to the token |

| Price behavior | Meme-like, needs new buyers | No token to price | Buyback-backed floor, but amplified swings |

| Who bears the risk | YT and token holders | The staker, transparently | Token holders, knowingly |

| Best for | Almost nobody | User-first, no-VC teams | Projects ready to become on-chain equity |

Structure Two's upside is that the token finally is a share: dividends get cleaner, and buybacks put a profit-backed floor under the price. Its downside is just as clear — the price now swings with the market and tracks Bitcoin, so a user who only wanted a steady yield is served well only in the early seasons, before the vault yield is phased out.

Where This Leaves Us

Today's yield-dividend governance token is mispriced by design. It doesn't carry meaningful governance — the BonkDAO drain and the Aave Labs standoff both show how little the vote is worth when the team writes the code and nobody shows up — and it doesn't carry a meaningful dividend, because the yield already belongs to the vault. Coin does not equal share, and the value-capture is badly mismatched. Retiring the token is the honest answer for user-first teams; migrating the yield into the token over several seasons is the ambitious one, converting a meme into equity at the cost of strapping the holder to Bitcoin's volatility. Both are trade-offs, not free wins.

I don't think there's one right answer here — but I'm fairly sure the current default, a token that neither governs nor pays, is the wrong one. What do you think? Leave your take in the comments.

This article is analysis and opinion, not financial advice. Protocol mechanics, revenue splits, and governance rules change frequently — verify the current design and risks yourself before committing capital.

Frequently asked questions

What is a yield-dividend DeFi protocol?+

It's a protocol that wraps a stablecoin around an ERC-4626 vault: a base token (ABC) holds the peg, and a staked wrapper (sABC) pays a steady 5-20% yield. The returns come from basis trades (Ethena's USDe, Falcon's USDf) or real-world assets (USDai, tokenized Treasuries). The model raises money from crypto, deploys it somewhere that earns, and repackages the yield as a product paying slightly more than a T-bill.

Do yield DeFi protocols actually need a governance token?+

Often not. In a yield-dividend protocol the revenue already flows to the 4626 vault, so the token carries little dividend right, and DAO votes execute inside code the team wrote, so it carries little real governance power. That leaves a token that neither governs nor pays — closer to a meme than equity. A protocol can pay a clean dividend and let users vote with their vault stake instead.

Why is a DeFi governance token often mispriced?+

Because governance and cash flow live on different channels. The token votes inside a fence the team built, so its governance power is nominal, while the protocol's yield is already committed to the 4626 vault, so its revenue right is thin. Holders absorb the volatility that the fixed-rate PT buyer sheds, without the control or the dividend to justify it — a structural value-capture mismatch, not an accident.

What happened in the BonkDAO governance attack of 2026?+

In July 2026 an attacker drained roughly $20M from BonkDAO's treasury without exploiting a bug. They spent about $4.4M buying just over 1% of BONK to control ~99.9% of votes cast, then submitted proposal BIP #76 to move the treasury to their wallet. It sat open ~6 days; when it executed on July 6, only seven wallets had voted (about 2.9% turnout). It shows how buyable token-weighted governance can be when nobody participates.

How could DeFi tokenomics turn a governance token into real equity?+

One design runs a fixed multi-season transition that shifts yield from the vault to the token — e.g. vault/token splits of 100/0, 80/20, 60/40, 40/60, then 0/100 across five seasons. By the end all revenue accrues to the token, the team holds a designed allocation instead of skimming yield, and points convert into that token. The token gains both governance and a dividend right, at the cost of price swings that track Bitcoin.

Is buying the PT of a yield protocol low risk?+

Relatively, yes — Pendle's PT locks a fixed rate and sheds most of the variable risk, which is why it's close to low-risk, high-return today. But that risk doesn't vanish; it lands on the YT holders and the governance-token holders, who absorb the volatility. The safest seat paying well while the protocol's own token bears the swings is exactly the mismatch this article argues yield protocols should fix.

About the Author

Practitioner turned analyst tracking how incentives, liquidity, and capital flows shape DeFi protocols.