AI data centers need hundreds of billions in capital that banks are too slow to lend, while GPUs lose a fifth of their value every year. USD.AI closes that gap with GPU-backed loans and pays the interest to depositors. Here's how the protocol works, where the risk really sits, and the four ways to participate — ranked.

Most "AI plays" in crypto are a ticker and a narrative. USD.AI is one of the few that is actually wired to the machine: it lends real dollars against real GPUs, collects interest from the operators renting those GPUs out, and passes that interest to depositors. No token emissions dressed up as yield — just credit.

That makes it more interesting than most protocols, and also harder to evaluate. This piece walks through why the opportunity exists, how the three core mechanisms fit together, where the risk genuinely sits, and the four concrete ways to participate — ranked from most conservative to most speculative.

A note on data: the protocol figures below (APYs, loans deployed, token stats) are a snapshot as of mid-2026. Yields, utilization, and the CHIP price move quickly here — treat the exact numbers as a point-in-time reading, not a live quote, and check USD.AI's dashboard before deploying.

1. Why GPU Financing Is a $100B+ Problem

To understand why USD.AI exists, you have to understand the scale of capital pouring into AI infrastructure — and why so much of it can't be met by traditional finance.

The numbers are staggering. In 2025 the four largest hyperscalers — Amazon, Microsoft, Alphabet, and Meta — collectively spent over $400 billion in capex, most of it on AI data centers. For 2026 the combined figure is projected to clear $700 billion. Analysts expect the tech sector to issue well over a trillion dollars in new debt over the coming years just to fund the build-out — hyperscalers alone floated hundreds of billions in bonds in the first half of 2026. Beneath them sits an entire tier of neoclouds — CoreWeave, Nebius, Lambda, Crusoe, IREN and dozens of smaller operators — building GPU clusters at institutional scale but without the credit history or balance sheet to raise bank financing quickly.

The supply side makes it worse. Nvidia's latest chips — H200, B200, B300, GB200 NVL72 — remain in critically short supply, sold out through much of 2026. On-demand rental capacity is essentially gone. One-year H100 contract prices climbed roughly 40% between late 2025 and early 2026 (to around $2.35/hr), and customers have been competing to pay well into the double digits per hour for B200 spot instances. For an operator with the hardware, the economics are compelling: at peak-scarcity rates a well-utilized H100 cluster could pay itself back in under two years and throw off six figures per GPU per year — and even at today's more normalized rates, contracted compute earns strong risk-adjusted returns for operators with creditworthy tenants locked in.

So the demand for capital is enormous and the assets throw off real cash. Why can't operators just borrow?

Because the clock doesn't cooperate. A traditional bank takes 12–24 months to underwrite a GPU loan; even a nimble private-credit fund takes 6–12. Meanwhile GPUs depreciate at roughly 20% a year with a useful life of only 3–4 years. By the time a conventional lender finishes due diligence, a large slice of the asset's productive value is already gone. That mismatch — fast-decaying collateral, slow-moving credit — is the gap USD.AI is built to close, targeting a 10–15% annual rate on GPU-backed loans in exchange for financing that arrives in weeks, not quarters.

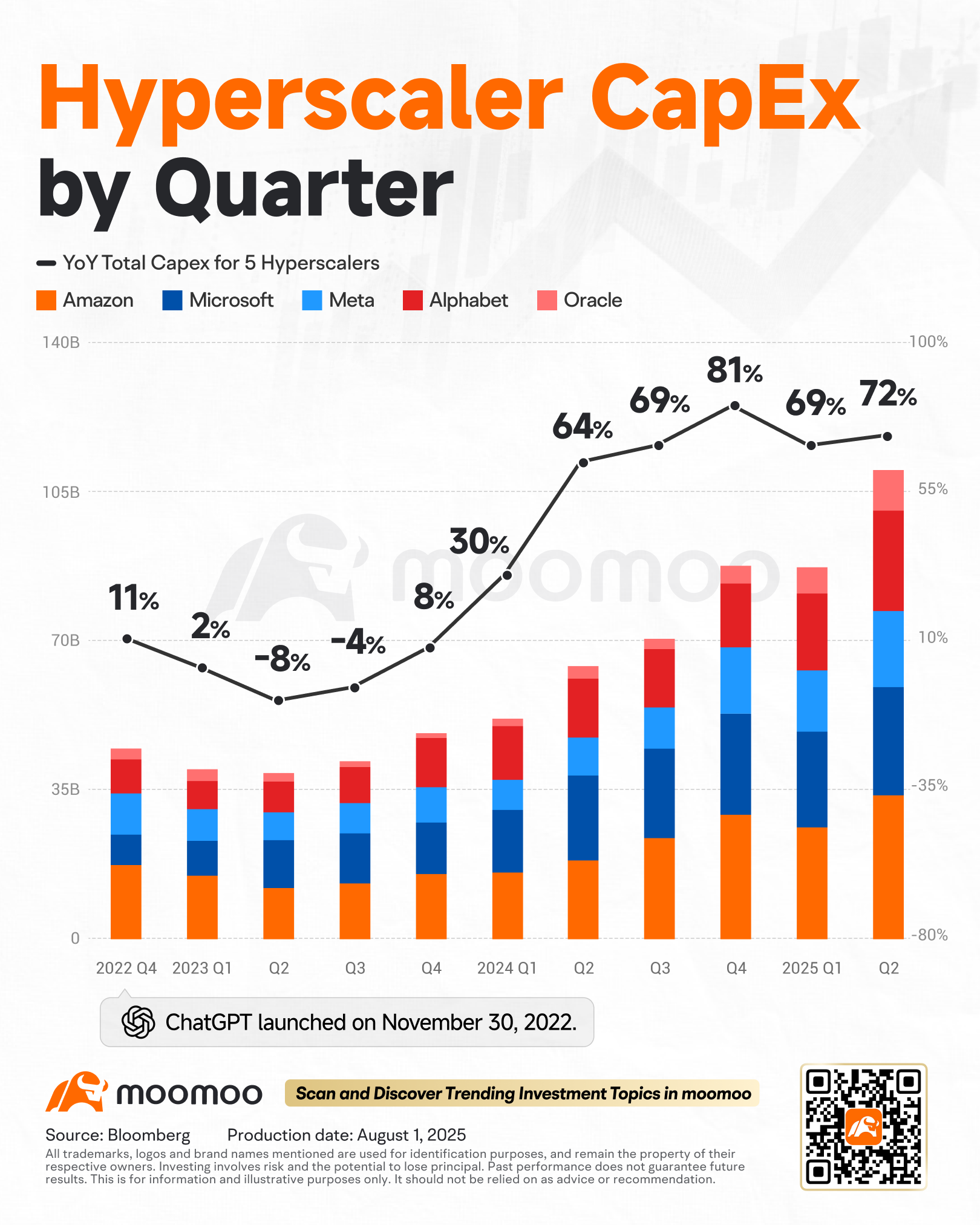

Hyperscaler capex has compounded relentlessly since late 2022 — year-over-year growth ran 64–81% through 2025. That spend has to be financed, and it flows all the way down to the neoclouds USD.AI lends to. (Source: Bloomberg / moomoo.)

Hyperscaler capex has compounded relentlessly since late 2022 — year-over-year growth ran 64–81% through 2025. That spend has to be financed, and it flows all the way down to the neoclouds USD.AI lends to. (Source: Bloomberg / moomoo.)

2. How the Protocol Works

USD.AI is a two-sided, on-chain credit market built primarily on Arbitrum, with liquidity also on Base. On one side, AI infrastructure operators borrow against their GPU fleets. On the other, depositors supply stablecoins and earn the interest that loan book throws off — without ever originating, underwriting, or managing a single loan.

- Borrowers are neoclouds, data centers, and GPU-as-a-service providers. Loans are non-recourse (recourse limited to the collateral, with a "springing recourse" clause that attaches to the corporate entity in fraud cases), amortized over 3 years, and issued at 70–80% LTV — a ~25% equity cushion from day one. Eligible hardware includes RTX Pro 6000, H200, B200/B300, and GB200/GB300.

- Depositors mint USDai with stablecoins, then stake it for sUSDai to earn.

Three primitives make this work — and each solves a problem that has sunk lesser RWA protocols.

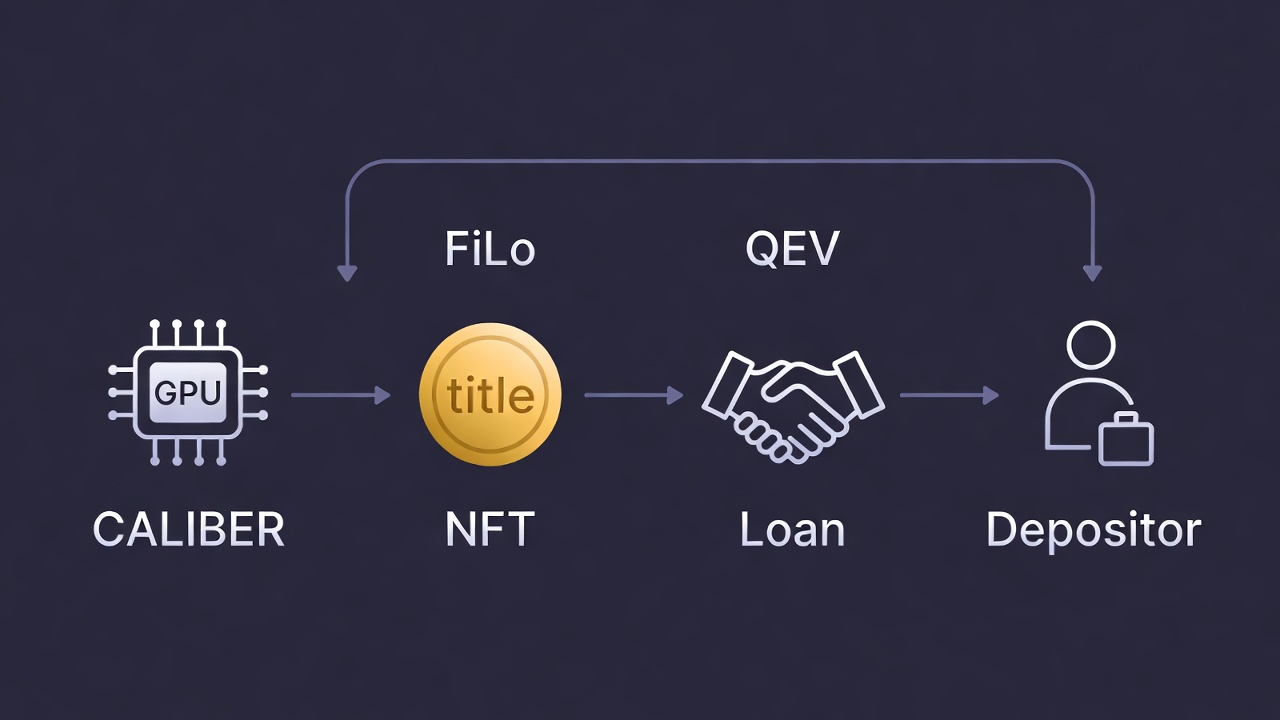

The whole loop in one line: CALIBER turns a physical GPU into an NFT title, FiLo curators underwrite the loan against it, and repayments flow back to depositors — with QEV governing how quickly they can exit.

The whole loop in one line: CALIBER turns a physical GPU into an NFT title, FiLo curators underwrite the loan against it, and repayments flow back to depositors — with QEV governing how quickly they can exit.

CALIBER — putting a physical GPU on-chain

You can't lend against a GPU you can't legally seize. CALIBER is the bridge that turns a physical chip into enforceable on-chain collateral. Each financed GPU is stored in an insured data center, documented under U.S. commercial law (UCC Article 7), and tokenized as an NFT — an Electronic Document of Title representing a legally enforceable claim to that specific hardware. Loans are issued against these NFT receipts. The chain of dependencies is worth stating plainly: without insurance there's no CALIBER, and without CALIBER there's no credible collateral — because in a default, physical repossession and resale is the recovery mechanism.

FiLo Curators — underwriters with skin in the game

FiLo (First Loss) Curators are the underwriting layer. They originate and structure individual loans, but they must post their own first-loss capital before a loan funds. In a default, the curator's money is wiped out before ordinary depositors take a cent of loss. The incentive is clean: a curator only profits when its borrowers perform, so the diligence — verifying hardware location, insurance, offtake contracts, revenue stability, borrower credit — is done with their own capital on the line. It's the same logic that makes a good protocol team's incentives worth reading, applied to loan origination.

QEV — pricing liquidity instead of promising it

This is USD.AI's most novel design, and it targets the fatal flaw of every RWA lender: depositors can want out at any moment, but the underlying loans are 3-year amortizing instruments. Rather than dangle a fragile promise of instant redemption, USD.AI prices liquidity instead of promising it:

- Redemption requests enter a FIFO queue, processed each 30-day epoch as borrower repayments flow in.

- On top of that queue sits QEV (Queue Extractable Value) — an auction layer where anyone who needs out faster can pay a premium to jump ahead, and that premium compensates the patient depositors still waiting behind them.

Together they convert a potential bank run into an orderly, time-priced exit by design. The honest caveat: protocol utilization is still climbing — a meaningful chunk of deposits sits in tokenized Treasury bills rather than active loans — so the queue has not yet been stress-tested under real redemption pressure. Elegant in theory; unproven under fire. As origination scales toward the multi-billion-dollar facility pipeline, this mechanism's real-world behavior is the single most important thing to watch.

3. The Three Tokens

USD.AI runs on three tokens with sharply different jobs. Confusing them is the most common way newcomers misjudge the risk.

| Token | What it is | Yield? | Role & risk |

|---|---|---|---|

| USDai | Synthetic dollar backed by a reserve of PYUSD (PayPal's regulated stablecoin), tokenized T-bills, and the GPU loan book | No | The liquid entry point — stable and composable, but inert. Think of it as the checking account. |

| sUSDai | What you get when you stake USDai | Yes — the yield lives here | Primary credit instrument for depositors. Value accrues into the USDai:sUSDai exchange rate (like ETH:stETH). Unstaking runs through the 30-day redemption queue. |

| CHIP | Governance token (USD.AI Foundation, Cayman), launched Q1 2026 via CoinList | Points + possible yield share | Governs collateral rules, rate tiers, fees. Staked sCHIP is the insurance backstop — it can be slashed to cover shortfalls. |

A few things worth internalizing:

sUSDai yield has two engines. It earns loan interest from GPU borrowers plus T-bill yield on idle reserves. As of mid-2026 the blended APY sat around ~8%, still depressed because a large share of capital is parked in T-bills while the loan pipeline ramps — and because unstaked USDai holders forgo yield, the pool concentrates among sUSDai holders. When a new loan settles, APY tends to spike then decay, since GPU loans are interest-first amortizing. As utilization rises, blended yield is targeted at the protocol's ~10–15% lending range. On top of that, PayPal provides a 4.5% incentive on PYUSD held in the protocol (a one-year program covering up to $1B of loan backing), which flows through into sUSDai yield. This is exactly the yield-dividend structure I've written about before — a base token that holds the peg, a staked wrapper that pays.

CHIP's dual nature is the trap. sCHIP earns points and votes, but it is also the last-resort deficit coverage — if loan losses exceed reserves, staked CHIP gets slashed. You are being paid to underwrite the protocol, not just to hold a governance token. Supply is 10 billion, split 27.5% ecosystem / 29.5% investors / 23.5% core contributors / 19.5% reserves, with investor and contributor tranches on a 12-month cliff. One underappreciated nuance: Season 1 was allocated 10% of supply, but the CoinList ICO didn't sell out — actual Season 1 distribution was closer to 5.6%, so real unlock pressure from the community round is materially lower than the headline suggests.

4. Where the Risk Actually Sits

USD.AI is a credit protocol, so it carries credit risk. Naming it precisely matters more than a generic "DYOR."

Asset–liability mismatch. Depositors want flexibility; the loans are 3-year instruments. QEV manages this architecturally but doesn't erase it — in a stress scenario the only real lever is the monthly cadence of borrower repayments, so queue times stretch.

Bank-run cascade. A high-profile default, a CHIP price collapse, or a wave of bad press could trigger simultaneous redemptions that overload the queue. The design turns a run into a slow, orderly process — but "orderly" still means waiting, and a 30-day queue feels like an eternity to someone who needs liquidity now.

The AI bubble — the existential one. The entire thesis rests on AI compute demand staying strong enough to keep rental rates and operator revenues high enough to service debt. If the AI capex cycle turns, the whole chain breaks: rental rates fall → operators miss payments → defaults rise → GPU resale values crater → collateral coverage drops below LTV → FiLo buffers get consumed. Even with clean legal title through CALIBER, repossessing and liquidating GPU clusters is slow, expensive, and depends on a functioning secondary market for the hardware. Underwriting assumes roughly 17% annual H100 depreciation; a next-gen obsolescence cliff from Nvidia could make that far too optimistic.

Everything else. Smart-contract bugs (audited, not immune); an evolving regulatory backdrop for synthetic dollars and RWA; governance centralization (investors + contributors hold ~53% of CHIP); and the explicit, by-design risk that sCHIP stakers lose capital in a shortfall.

Credit where due — the mitigations are unusually thoughtful for the category:

| Risk vector | How USD.AI addresses it |

|---|---|

| Collateral authenticity | CALIBER: UCC Article 7 electronic-title NFTs; insurance required on every GPU |

| Credit default | FiLo first-loss capital absorbs losses before depositors |

| Mass redemption | QEV converts panic into time-priced, orderly exits |

| Overcollateralization erosion | 70–80% LTV at origination; 3-year amortization designed to outrun depreciation |

| Oracle manipulation | Oracle-free architecture — no external price feed, no flash-loan attack surface |

| Extreme loss | sCHIP insurance module as last-resort deficit coverage |

| Idle capital | T-bill yield on undeployed reserves provides a yield floor |

The PayPal/PYUSD relationship adds real institutional scaffolding: a regulated, NYDFS-supervised stablecoin at the core, plus an incentive that effectively subsidizes borrower cost of capital and widens credit access for smaller operators.

5. How to Participate — Four Strategies, Ranked

Here's the whole map, from most conservative to least. My priority ranking is unambiguous: hold sUSDai → LP on Pendle/DEX → farm the Allo Game → buy CHIP outright.

| Strategy | Effort / risk | What you earn | Best for |

|---|---|---|---|

| 1. Hold sUSDai | Low | ~8% now, target ~10–15% real yield | Stablecoin savers wanting AI-credit exposure |

| 2. Pendle / DEX LP | Medium | ~5% LP yield + Allo Points | Intermediate users wanting yield + airdrop optionality |

| 3. Farm the Allo Game | High | CHIP airdrops, 1x–40x multipliers | Experienced farmers who actively manage positions |

| 4. Buy & stake CHIP | High / speculative | Points + governance (yield TBD) | Long-term conviction holders only |

Strategy 1 — Hold sUSDai (most conservative)

Acquire stablecoins, mint USDai at app.usd.ai, stake it for sUSDai, and the yield accrues automatically in the exchange ratio. New users can apply referral code UT8X0 at sign-up. Your exposure is to the protocol's credit quality and GPU-market conditions; redemptions run through the 30-day redemption queue. The key virtue: the yield is sourced from real loan interest, not token emissions. Best for stablecoin savers who want real-yield exposure to AI infrastructure and can tolerate limited short-term liquidity.

Strategy 2 — Pendle / DEX LP (the balanced middle)

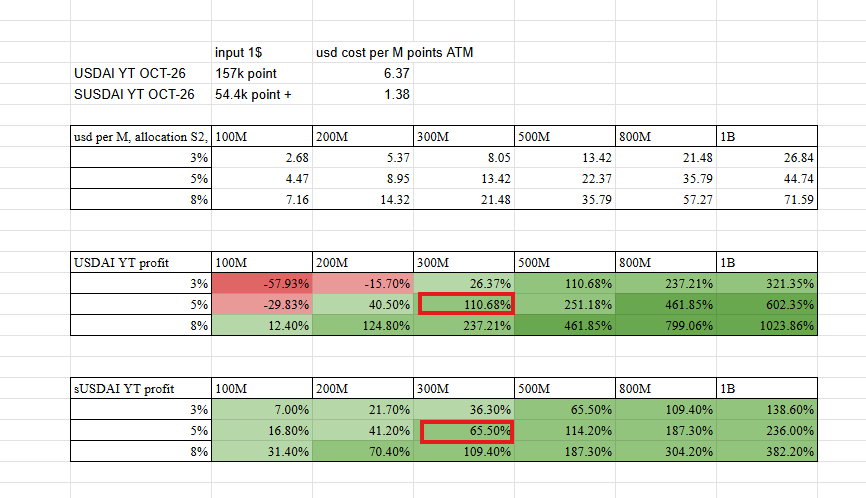

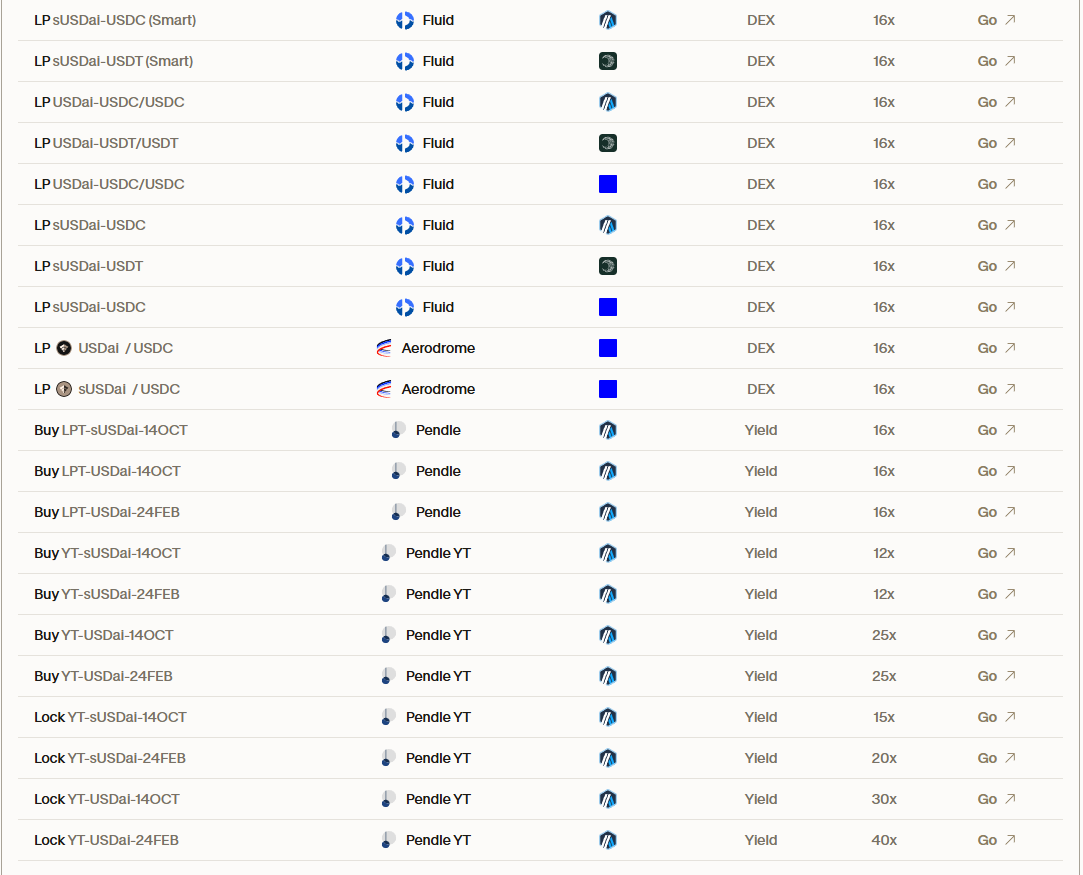

USD.AI's primary DeFi liquidity lives on Pendle (Arbitrum), with stable pairs also on Aerodrome (Base). Providing LP earns trading fees plus Allo Points at a higher multiplier than simple holding. LP is less risky than buying Pendle YT outright — an LP position holds both PT and YT, and the PT leg provides a floor value at maturity. Base LP APY is modest (~5%), but stacked with points the total return can be meaningful depending on where CHIP eventually settles. Multipliers decay over time, so earlier deposits lock in better rates. Impermanent loss on stablecoin-heavy pairs is minimal. To sanity-check point returns before committing, use the USD.AI point calculator.

Point returns are a function of two unknowns — how many points you accrue and what CHIP is ultimately worth. Modelling it across a grid of airdrop-allocation and FDV assumptions (green = profit, red = loss) is the honest way to size a farm, rather than trusting a single headline APY.

Point returns are a function of two unknowns — how many points you accrue and what CHIP is ultimately worth. Modelling it across a grid of airdrop-allocation and FDV assumptions (green = profit, red = loss) is the honest way to size a farm, rather than trusting a single headline APY.

Strategy 3 — Farm the Allo Game (high risk / high reward)

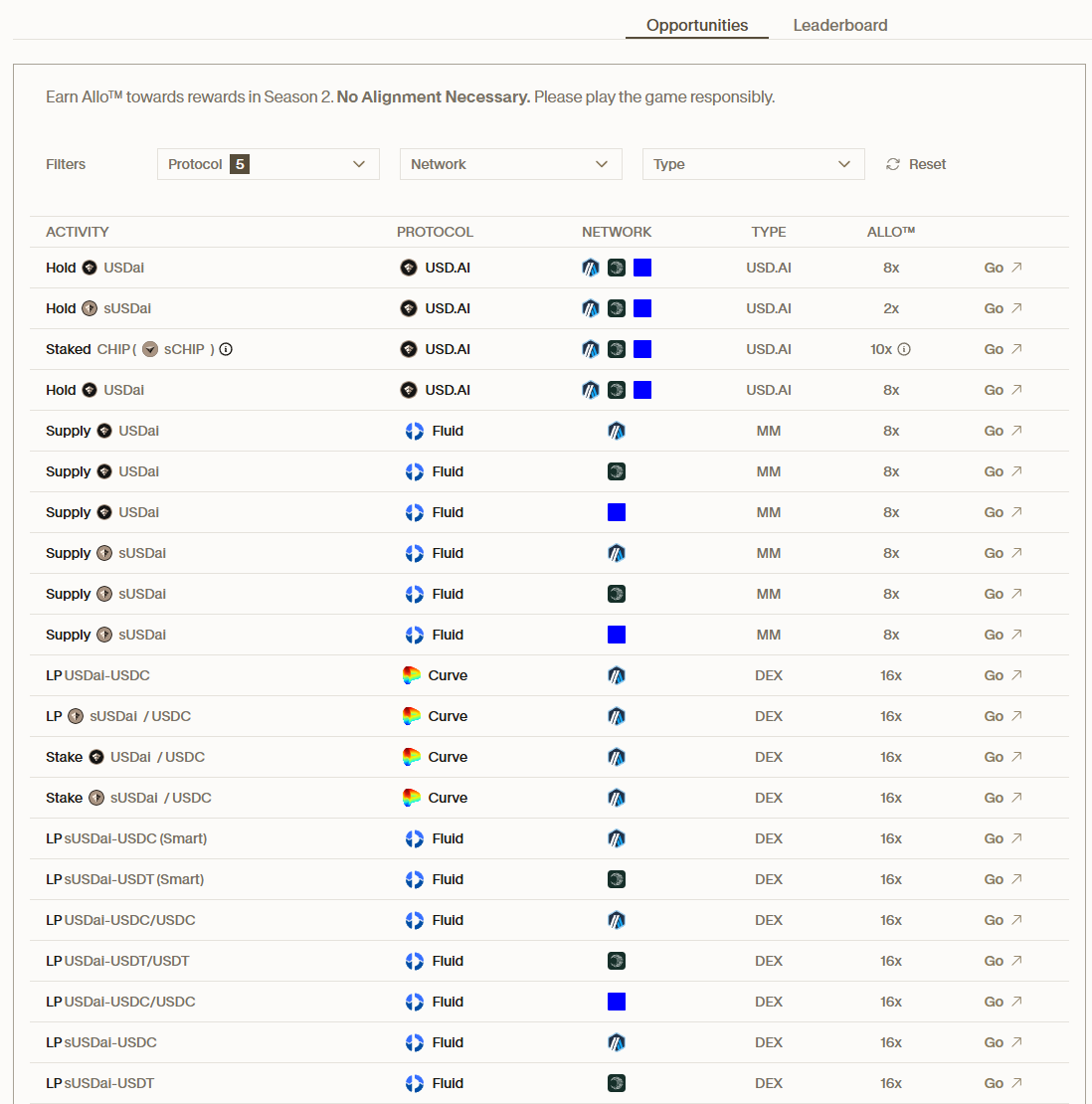

The Allo Game is USD.AI's points program; Season 1 has concluded and Season 2 (Flatiron) is live, with rewards distributed as CHIP airdrops and multipliers from 1x to 40x. The live opportunity list lives at app.usd.ai/rewards and changes often, so check before deploying.

The base of the Allo board: simply holding USDai earns 8x and sUSDai 2x, staked CHIP 10x, while stablecoin LP on Curve and Fluid jumps to 16x. Multipliers reward the activities the protocol most wants — deeper liquidity over passive holding.

The base of the Allo board: simply holding USDai earns 8x and sUSDai 2x, staked CHIP 10x, while stablecoin LP on Curve and Fluid jumps to 16x. Multipliers reward the activities the protocol most wants — deeper liquidity over passive holding.

The main plays:

- Hold sUSDai — base points, low effort.

- LP USDai/USDC on Pendle or a DEX — higher multipliers than holding.

- Split sUSDai into PT and YT on Pendle, then loop the PT as collateral in a lending protocol for amplified exposure.

- Refer users — your wallet earns 10% of all points generated by wallets you refer; content creators can apply for up to a 100% referral boost.

The top of the ladder is Pendle: buying and locking YT-USDai can reach 25x–40x. That is also where the risk concentrates — those multipliers exist precisely because YT is the most dangerous seat in the trade.

The top of the ladder is Pendle: buying and locking YT-USDai can reach 25x–40x. That is also where the risk concentrates — those multipliers exist precisely because YT is the most dangerous seat in the trade.

The risks are real: Pendle YT is pure interest-rate speculation and can decay toward zero at maturity; Allo Game rules and multipliers have changed meaningfully between seasons; and CHIP's secondary market is volatile. This is the same point-farming discipline that applies everywhere — treat points as an editable database entry, not a guaranteed token. Best for experienced mercenary capital that understands Pendle mechanics and can actively manage.

Strategy 4 — Buy & stake CHIP (not recommended right now)

CHIP is live and widely listed (Binance, Coinbase, Bybit, OKX and more), and staking gives sCHIP that accrues Season 2 points. I don't recommend it as a primary strategy today, for three reasons.

CHIP's price tells the story: a launch spike toward $0.12, then a steady bleed to around $0.031 — down roughly 78% from its April high, and about 51% year-to-date. Rational for a token that, so far, carries only points and governance. (Source: CoinGecko.)

CHIP's price tells the story: a launch spike toward $0.12, then a steady bleed to around $0.031 — down roughly 78% from its April high, and about 51% year-to-date. Rational for a token that, so far, carries only points and governance. (Source: CoinGecko.)

First, the utility is under-specified — the team hasn't published detailed sCHIP reward structures, yield-distribution parameters, or slash conditions, so valuing the token on fundamentals is guesswork, and buying what you can't model is a bet, not an investment. Second, unlock pressure is real — investor and contributor tranches (~53% combined) began unlocking at month 12 and continue through 2026–2027 from well-capitalized, low-cost-basis holders. Third, the tape has been brutal — CHIP is down roughly 78% from its April 2026 all-time high, a slow bleed that makes sense for a token carrying no dividend right and, so far, only points and governance. None of this means CHIP is a bad long-term bet; it may appreciate significantly if the protocol executes. But until the team documents sCHIP mechanics clearly, sizing a meaningful position is speculation. Best left to long-term conviction holders with defined risk limits.

If you find this guide useful and decide to participate, referral code UT8X0 is available — it costs you nothing, doesn't affect your own point earnings, and is entirely optional.

6. Where Things Stand (mid-2026)

- Funding: $13M Series A led by Framework Ventures, plus $4M from Bullish; a strategic investment from EchoStar/DISH into Permian Labs followed in mid-2026.

- Loan book: north of $800M in signed term sheets and a multi-billion-dollar borrower pipeline; roughly $200M+ closed and deployed across active loans (the largest, ~$98M, financing 2,300+ B300s for Duos Edge AI), against headline facilities of $500M each with Sharon AI and QumulusAI plus selection for OBEX's inaugural $1B cohort.

- TVL: grew past $600M at peak; on-chain TVL sits in the low hundreds of millions with more capital deployed off-chain in loans.

- Integrations: Pendle (Arbitrum), Aerodrome (Base), Morpho, Fluid, Euler, Curve, Uniswap V4 — including a $100M sUSDai liquidity facility on Fluid.

- CHIP: live and widely listed across major exchanges; Season 2 (Flatiron) active, scheduled to run through October 2026.

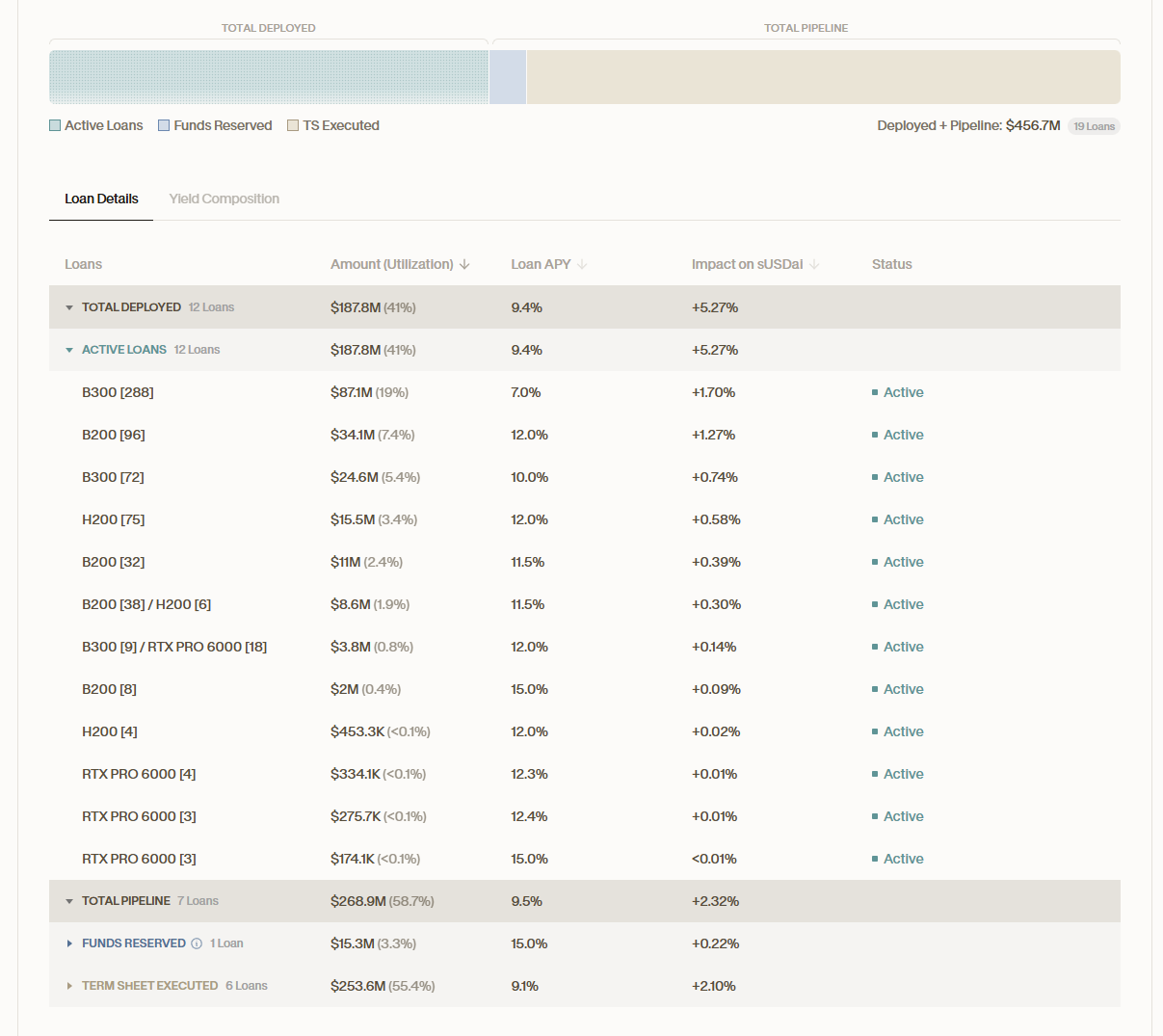

The live loan book is fully transparent: roughly $188M deployed across active loans (about 41% utilization) at a blended ~9.4% loan APY, broken out by GPU model — B300, B200, H200, RTX Pro 6000 — with the pipeline visible alongside. This is the on-chain equivalent of reading a lender's book line by line.

The live loan book is fully transparent: roughly $188M deployed across active loans (about 41% utilization) at a blended ~9.4% loan APY, broken out by GPU model — B300, B200, H200, RTX Pro 6000 — with the pipeline visible alongside. This is the on-chain equivalent of reading a lender's book line by line.

7. The Bottom Line

USD.AI occupies genuinely differentiated territory. It isn't an algorithmic stablecoin, a governance token selling a story, or a plain yield aggregator — it's a structured credit protocol with real borrowers, real hardware collateral, and real interest reaching depositors. That's the bull case: verifiable yield sourced from loan repayments rather than inflation, a structural and growing financing gap, credible institutional backing (Framework, PayPal/PYUSD, listed neocloud borrowers), and a three-layer risk architecture (CALIBER + FiLo + QEV) more sophisticated than most RWA peers.

The bear case is equally clear: the whole book is hostage to the AI capex cycle; physical GPU liquidation is slow and legally messy; the redemption queue has never been tested at scale; and today's ~8% yield still leans on a "low-to-mid teens when fully deployed" thesis that depends on the pipeline actually executing. Size your participation to how much of that thesis you actually believe — and start at the conservative end of the ladder.

This article is for informational purposes only and is not investment advice. Crypto and RWA protocols carry significant risk; do your own research and only participate with capital you can afford to lose. The referral code reflects the author's own participation and has no effect on the reader's point earnings.

Frequently asked questions

What is USD.AI and how does it generate yield?+

USD.AI is an on-chain credit protocol that lends stablecoins to AI infrastructure operators — neoclouds and data centers — secured by their GPU fleets. Borrowers pay 10-15% annual interest on 3-year, 70-80% LTV loans; that interest, plus Treasury-bill yield on idle reserves, flows to depositors who stake USDai for sUSDai. The yield is real loan interest, not token emissions, which is what separates it from most 'AI' crypto plays.

What is the difference between USDai, sUSDai, and CHIP?+

USDai is a synthetic dollar backed by a reserve of PayPal's PYUSD, tokenized Treasury bills, and the GPU loan book — liquid and composable but it earns no yield on its own. sUSDai is what you get when you stake USDai; it is the yield-bearing token, with value accruing into the exchange rate like stETH. CHIP is the governance token: staked as sCHIP it earns points and votes, but it also serves as the insurance backstop and can be slashed to cover loan losses.

How does USD.AI turn a physical GPU into on-chain collateral?+

Through CALIBER. Each financed GPU is stored in an insured data center, documented under U.S. commercial law (UCC Article 7), and tokenized as an NFT — an Electronic Document of Title representing a legally enforceable claim to that specific hardware. Loans are issued against these NFT receipts. Insurance is mandatory, because in a default the recovery mechanism is physically repossessing and reselling the GPU, so the hardware must be seizable and salvageable.

Can you withdraw from USD.AI instantly?+

No — redemptions run through a FIFO queue processed every 30-day epoch as borrower loan repayments flow in. On top of it sits QEV (Queue Extractable Value), an auction layer where anyone needing out faster can pay a premium to jump ahead, and that premium compensates patient depositors still waiting. It converts a potential bank run into an orderly, time-priced exit. Utilization is still ramping, so the queue has not yet been stress-tested under real redemption pressure.

What APY does sUSDai pay?+

As of mid-2026 the blended sUSDai APY sat around 8%, depressed because a large share of capital is still parked in tokenized Treasury bills while the loan pipeline ramps. As GPU-loan utilization rises, blended yield is targeted at the protocol's 10-15% lending range. A PayPal incentive of 4.5% on PYUSD held in the protocol flows through on top. Yields move fast here, so treat any figure as a point-in-time reading.

What is the biggest risk of using USD.AI?+

The AI capex cycle. The entire loan book assumes GPU rental rates and operator revenues stay high enough to service debt. If demand reverses, operators miss payments, defaults rise, GPU resale values fall, collateral drops below LTV, and FiLo first-loss buffers get consumed. Secondary risks include the untested QEV queue in a mass redemption, slow physical liquidation of hardware, and sCHIP slashing — staked CHIP can lose capital by design in a shortfall.

About the Author

Practitioner turned analyst tracking how incentives, liquidity, and capital flows shape DeFi protocols.